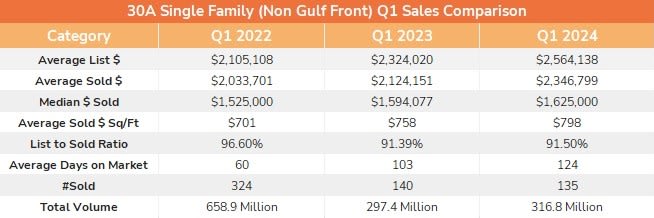

Analyzing the provided statistics for the 30A Single Family (Non Gulf Front) market, we can offer insights into the Q1 performance over the past three years:

Q1 2022 - Q1 2023: A Market in Flux

- Average Listing and Sold Prices: There was an upward trend in both the average list and sold prices, which may suggest an increase in buyer confidence or a response to a limited supply of non-gulf front homes.

- Median Sale Price: The median sale price saw an increase, reinforcing the demand for single-family homes in this desirable area.

- Average Sold Price per Sq/Ft: The average price per square foot also rose, indicating a market that was willing to pay more for premium non-gulf front real estate.

- List to Sold Ratio: The slight decrease in the list to sold ratio might reflect a market where buyers started to negotiate more, or where listings were initially priced more ambitiously.

- Average Days on Market: The number of days on market increased significantly, suggesting that while homes were selling for more, they were taking longer to close.

- Sales Volume: There was a dramatic decrease in total sales volume, possibly a result of fewer sales or a shift in the types of homes being sold.

Q1 2023 - Q1 2024: Resilience Amidst Adjustments

- Average Listing and Sold Prices: Prices continued to grow, albeit at a potentially unsustainable rate, which could reflect a mismatch between seller expectations and market reality.

- Median Sale Price: The median sale price saw a moderate increase, which might point to a continuing appreciation for well-placed properties despite broader market challenges.

- Average Sold Price per Sq/Ft: Continuing the upward trend, the cost per square foot increased, possibly due to improved home features or a continued premium on non-gulf front properties.

- List to Sold Ratio: The ratio dipped further, which could indicate a growing buyer's market where purchasers are in a stronger position to negotiate.

- Average Days on Market: Homes are now taking longer to sell, a clear sign of a market slowdown which could be a result of higher prices tempering buyer urgency.

- Sales Volume: The sales volume saw an increase from the previous year but remained significantly lower than in 2022, hinting at a market that is still finding its footing.

Analysis for Buyers and Sellers

- Buyers are in a stronger negotiating position than in previous years, with the luxury of more time and potentially more leverage due to the increased average days on market and lower sales volume.

- Sellers may need to adjust their pricing strategies and be prepared for longer selling periods, although the higher average sold prices indicate that with the right approach, the market can still yield favorable results.

Conclusion The 30A single-family non-gulf front home market has shown a pattern of rising prices and a slower pace, suggesting that while there's still demand for these homes, buyers are becoming more deliberate in their purchases. Sellers might have to align their expectations with the evolving market conditions to capitalize on their investments.

In this shifting landscape, our detailed understanding of these trends can offer a strategic advantage to our clients, ensuring they can make the most of their real estate endeavors in 2024 and beyond.